[elfsight_social_share_buttons id=”1″]

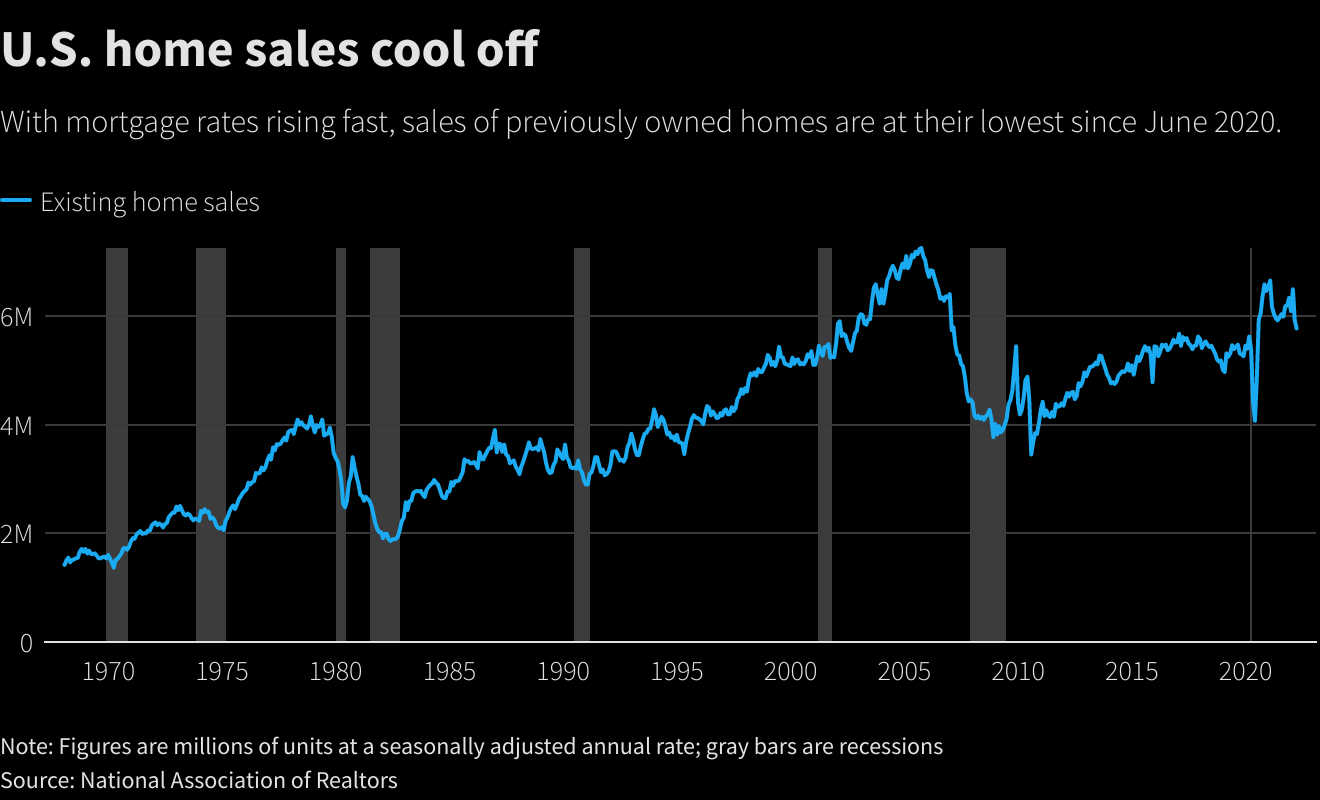

U.S. home sales dropped to the lowest level in nearly two years in March as house prices raced to a record high and could decline further with mortgage rates hitting 5%.

The report from the National Association of Realtors on Wednesday also showed the drop in sales in February was much steeper than initially thought.

Even with home sales reverting to their pre-pandemic level, the housing market remains hot. Homes sold in March typically stayed on the market for only 17 days and the share of all-cash sales was the largest in eight years.

“For the best chance of success, home shoppers should have cash offers ready, and they should lock in mortgage rates, as they are expected to keep rising,” said Robert Frick, corporate economist at Navy Federal Credit Union in Vienna, Virginia.

Existing home sales dropped 2.7% to a seasonally adjusted annual rate of 5.77 million units last month, the lowest level since June 2020. Data for February was revised sharply down to a rate of 5.93 million units from the previously reported 6.02 million units.

March sales mostly reflected the closing of contracts signed two to three months ago when the 30-year fixed-rate mortgage was below 4%. Economists polled by Reuters had forecast sales would decrease to a rate of 5.80 million units. Sales fell in the Northeast, South, and Midwest. They were unchanged in the West.

Home resales account for the bulk of U.S. home sales. They were down 4.5% on a year-on-year basis in March.

The 30-year fixed-rate mortgage averaged 5.0% during the week ended April 14, the highest since February 2011 and up from 4.72% in the prior week, according to data from mortgage finance agency Freddie Mac.

The Federal Reserve in March raised its policy interest rate by 25 basis points, the first-rate hike in more than three years, as the U.S. central bank battles surging inflation. Economists expect the Fed will hike rates by 50 basis points next month, and soon start trimming its asset portfolio.

Tight Market

The housing market is the sector of the economy most sensitive to interest rates. But with still low inventory, economists believe higher borrowing costs will have a moderate impact on demand.

While single-family homebuilding and permits fell in March, both remained at high levels. The inventory of single-family housing under construction was the highest since November 2006, government data showed on Tuesday.

Still, owning a home is becoming unaffordable for many Americans. The median existing house price jumped 15% from a year earlier to an all-time high of $375,300 in March. Sales remained concentrated in the upper-price end of the market.

The South, which has experienced an increase in migration from other parts of the country, recorded big price gains.

There were 950,000 previously owned homes on the market in March, up 11.8% from February, but down 9.5% from a year ago.

At March’s sales pace, it would take 2.0 months to exhaust the current inventory, down from 2.1 months a year ago. A six-to-seven-month supply is viewed as a healthy balance between supply and demand.

Properties typically remained on the market for 17 days last month, down from 18 days a year ago. Eighty-seven percent of homes sold last month were on the market for less than a month.

First-time buyers accounted for 30% of sales last month, up from 29% in February and down from 32% a year ago. Economists and realtors say a 40% share of first-time buyers is needed for a robust housing market.

All-cash sales made up 28% of transactions in March, the most since July 2014. That was up from 25% in February and 23% in March 2021. Individual investors or second-home buyers, who account for many cash sales, bought 18% of homes in March, up from 15% from a year ago.

Copyright 2022 Thomson/Reuters